Every leadership team faces the same problem. There are more project ideas on the table than capital, time, or people to deliver them. Someone has to decide which ideas move forward and which ones get parked. The hard part is making that call without falling back on the loudest voice in the room or the personal preference of whoever owns the budget.

The cost of getting these decisions wrong is well documented. CB Insights research on startup post-mortems shows that 42% of failed ventures had no real market need, 29% ran out of cash, and 23% failed because of team and execution issues. The US Bureau of Labor Statistics reports that 48% of new businesses fail within five years.

McKinsey research on large transformation programs has consistently shown that around 70% fall short of their stated goals. The pattern is consistent across startup ideas and corporate projects alike. Most failures are baked in at the decision stage, not the execution stage.

This guide explains how to run a business feasibility assessment that produces a defensible go or no-go decision. You will learn when to do a quick screen versus a full assessment, how to score project ideas across five dimensions, the red flags that should stop a project immediately, and how to present your findings to leadership in a way that drives action.

What is a Business Feasibility Assessment?

A business feasibility assessment is a structured evaluation that tests whether a proposed project, product, or initiative should move forward. It produces a clear recommendation backed by evidence, financial modeling, and risk analysis.

The output is not a long report. It is a decision. The assessment exists to answer one question: should we commit capital, people, and time to this idea, or not?

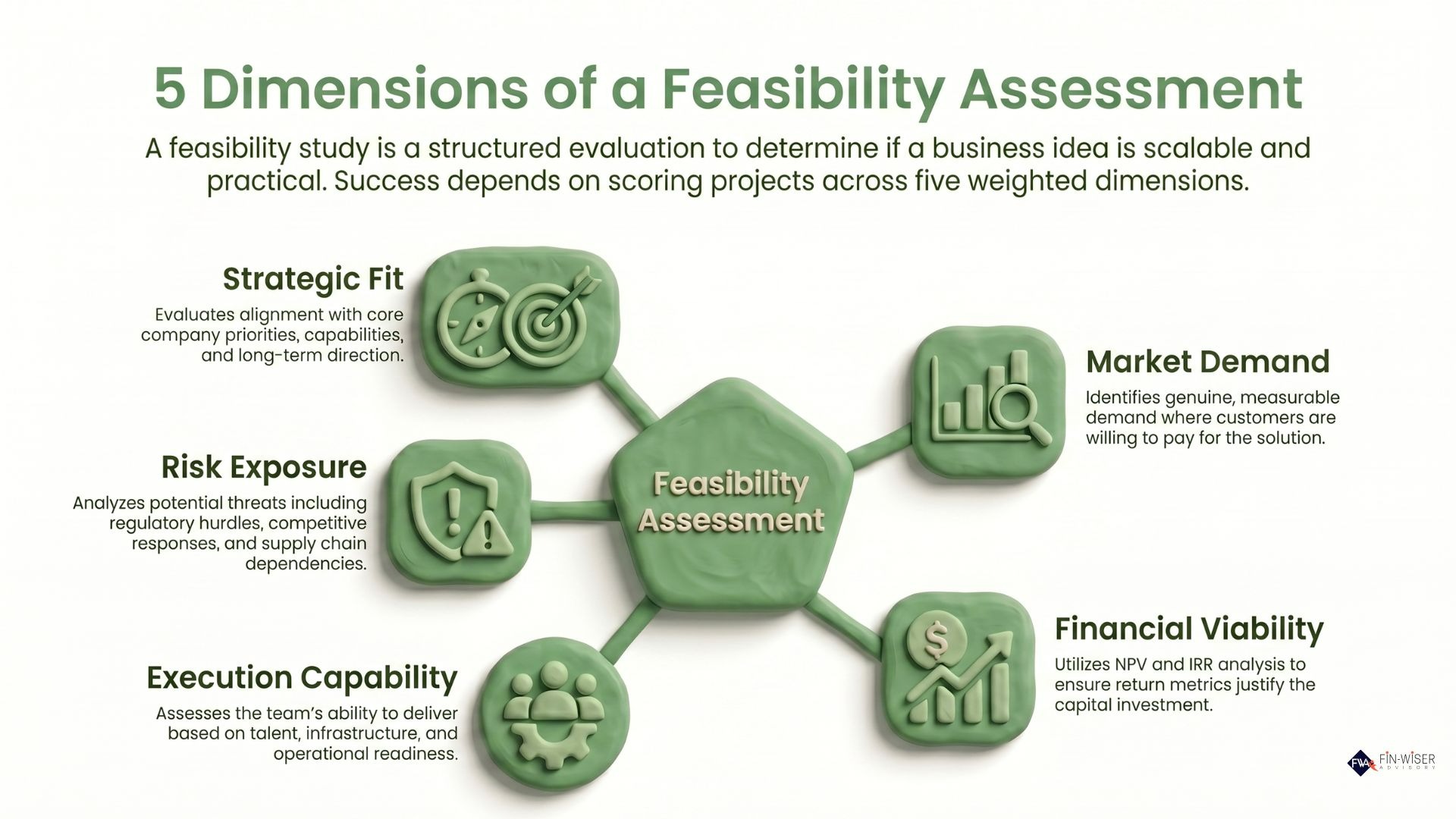

The 5 Dimensions to Score in a Feasibility Assessment

Most assessments fail because they treat every factor as equally important. They are not. A practical assessment scores ideas across five dimensions and weights them based on what matters most for that specific project.

Strategic Fit

Does this project align with company priorities, capabilities, and direction? A great idea in the wrong company is still a bad project.

Market Demand

Is there genuine, measurable demand? This is where most assessments fail. Surveys saying customers would buy something are not the same as customers actually paying for it.

Financial Viability

Will the numbers work? This means realistic revenue projections, defensible cost assumptions, and return metrics that justify the capital. Solid NPV and IRR analysis is the backbone of this dimension.

Execution Capability

Can your team actually deliver this? Strategy without execution capacity is fiction. Score this dimension on talent, infrastructure, and operational readiness.

Risk Exposure

What could go wrong, and how badly? This covers regulatory risk, competitive response, supply chain dependencies, and concentration risk.

Weighted Scoring Model: A Practical Example

A scoring model turns subjective judgment into a structured comparison. Each dimension gets a weight based on importance, and the project gets a score out of 10 on each dimension. Multiply, add, and you have a single number to compare against other projects.

A score above 7.5 typically signals a strong project. Between 6 and 7.5, the project is workable but needs specific improvements before approval. Below 6, the assessment should either send the idea back for rework or kill it.

The weights are not fixed. A regulated industry might push risk exposure higher. A growth-stage company might weight market demand and strategic fit more heavily. The model is a tool, not a rule.

Red Flags That Should Stop a Project Immediately

Some findings should kill a project regardless of the overall score. These are not weighted dimensions, they are pass-fail tests.

- No measurable demand signal. If no one has paid for a comparable solution and no credible research shows willingness to pay, the project does not move forward.

- Negative unit economics with no path to fix them. If the cost to acquire and serve a customer exceeds lifetime revenue and there is no realistic plan to reverse that, the project is unviable regardless of strategic appeal.

- Regulatory or legal blockers without mitigation. A project that cannot be licensed or operated legally in the target market is dead, full stop.

- Capital requirement that exceeds available funding by more than 25 percent. Stretched budgets fail. If the gap cannot be closed, the project gets parked or rescoped.

- Critical capability gap with no acquisition plan. If you do not have the talent and cannot reasonably hire or contract it, the project will fail in execution.

These red flags exist because some problems cannot be averaged away with strong scores in other dimensions.

Quick Screen vs Full Assessment: When to Use Each

Not every idea deserves the same level of scrutiny. Spending six weeks assessing a small initiative wastes resources, while running a quick screen on a major capital project creates dangerous blind spots. The right approach depends on the size of the commitment.

A quick screen looks for obvious deal-breakers. Is there clear demand? Do we have the basic resources? Is the financial logic plausible? If all three answers are yes, the idea graduates to a full assessment. If any answer is no, the project either gets killed early or sent back for rework.

How to Present Findings to Leadership

A great assessment that does not drive action is a wasted exercise. Most assessments fail at the presentation stage because they bury the decision in 80 pages of analysis.

A good leadership presentation has four parts. First, the recommendation, stated in one sentence at the top. Second, the three to five reasons that drove the recommendation, with the supporting evidence. Third, the key risks and how the team plans to manage them. Fourth, the specific decisions and resources required from leadership.

Leaders do not want to read the assessment. They want to know whether to fund the project, what they are risking, and what they need to decide. Structure the presentation around their decision, not your analysis.

If the answer is no-go, do not soften it. Clear nos save more capital than soft maybes. If the answer is go but with conditions, list the conditions explicitly so they become commitments.

Greenlight vs Redlight: What Each Outcome Looks Like

A greenlight outcome includes a defensible market signal, financial returns above the company hurdle rate, execution capacity confirmed by named owners, risks documented with mitigation plans, and a clear next-stage budget and timeline.

A redlight outcome looks different. The market signal is weak or theoretical. The financial returns either do not clear the hurdle rate or depend on assumptions that fail sensitivity tests. Execution capacity is missing or speculative. Risks are present without credible mitigation. The recommendation is to stop, rework, or wait for conditions to change.

The valuable assessments are the ones that produce clear redlight outcomes when warranted. Avoiding bad investments creates more value than chasing marginal good ones. For more on the modeling errors that drive false greenlights, see our breakdown of common modeling mistakes that have cost startups millions.

How Finwiserr Can Help

A business feasibility assessment is only useful if the analysis is rigorous and the recommendation is defensible under scrutiny. The financial model has to hold up when investors and lenders pull it apart, the market data has to be current, and the conclusion has to follow logically from the evidence.

At Finwiserr, we run feasibility assessments and build the financial models that support them. Our team has worked across renewable energy, real estate, manufacturing, hospitality, and infrastructure projects. We focus on what actually drives funding and approval decisions, including realistic revenue ramps, defensible cost assumptions, sensitivity analysis on the variables that matter, and clear risk disclosure. If you are evaluating a major project, preparing for a capital approval, or trying to bring discipline to your project pipeline, our project finance advisory team can help you build assessments that produce decisions, not just reports.

A short conversation early in the process often saves months of effort and significant capital.

FAQs About Business Feasibility Assessment

What scoring method works best for a business feasibility assessment?

A weighted scoring model across five dimensions works for most projects. Assign weights based on what matters for that specific project, score each dimension between 1 and 10, and calculate a weighted total. Anything above 7.5 typically warrants approval, while anything below 6 either needs rework or should be stopped.

Who should own a business feasibility assessment inside a company?

Ownership usually sits with the project sponsor, but the analysis itself should be led by an independent party such as a finance team, internal PMO, or external advisor. Founders and project sponsors are too close to the idea to assess it without bias, which is why lenders and investors typically require independent input.

How do you handle disagreement between stakeholders during an assessment?

Anchor the discussion on evidence, not opinion. When stakeholders disagree, identify which dimension drives the disagreement and what data would resolve it. If the disagreement is on weights, surface it explicitly so leadership can decide. Disagreement on weights is healthy, disagreement on facts means the analysis is incomplete.

What is the difference between a feasibility assessment and a feasibility study?

The terms are often used interchangeably, but in practice an assessment is the broader decision exercise, while a study is the detailed underlying research. An assessment uses the study as input and adds the scoring, recommendation, and stakeholder presentation that drive the actual decision.

Can you run a feasibility assessment on an existing project that is already underway?

Yes, and sometimes you should. If a project is missing milestones, burning capital faster than planned, or facing changed market conditions, a fresh assessment can answer whether to continue, pivot, or stop. This is sometimes called a stage-gate review and is standard practice in project finance and large capital programs.