Expatriates living and working in Dubai occupy one of the most financially advantageous positions in the world. There is no personal income tax. Salaries are competitive. The AED is pegged to the US dollar. Access to global markets is straightforward. And yet, a significant number of expats leave Dubai after ten or fifteen years with far less accumulated wealth than their income should have produced.

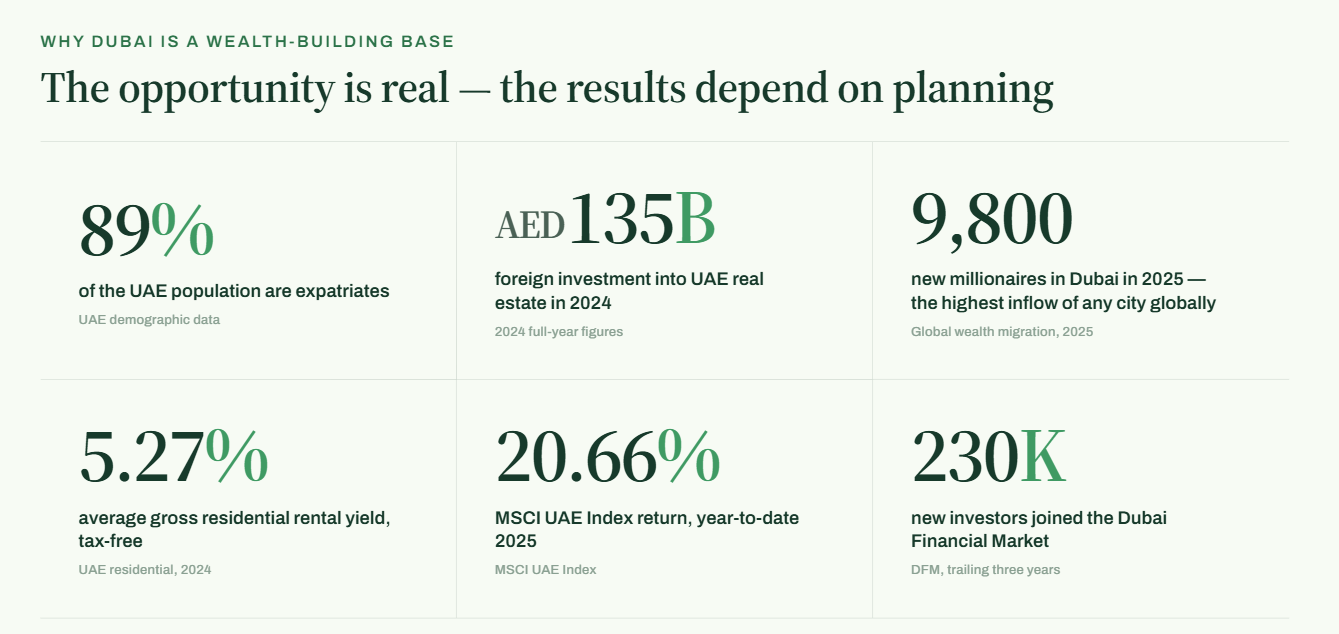

Expats make up 89% of the UAE’s population. In 2024 alone, foreign investors committed over AED 135 billion to UAE real estate. Dubai welcomed 9,800 new millionaires in 2025, the highest inflow of any city globally that year. The opportunity is real. The results, however, depend entirely on whether an individual has a structured plan.

The difference between those who leave wealthy and those who do not is rarely income. It is almost always planning.

This guide provides a practical, step-by-step framework for investment planning as a Dubai expat. It covers what to prioritise, what to avoid, and which tools actually deliver results.

Not sure what kind of financial professional you need? Finwiserr’s complete guide to financial advisors in Dubai explains exactly what advisors do, which qualifications matter, and the warning signs that cost expats money every year.

Why Investing in Dubai Requires a Different Approach

Investing as a Dubai expat is fundamentally different from investing as a resident in the UK, India, Australia, or the United States. The tax-free salary is a genuine advantage. However, it comes with structural realities that a standard home-country investment framework was not designed to handle.

| Challenge | Why It Matters for Dubai Expats |

| No state pension | The UAE offers no government pension. End-of-service gratuity rarely provides sufficient retirement income on its own. |

| Currency risk | Earning in AED but retiring in GBP, EUR, or INR means exchange rate movements over a decade can silently erode savings. |

| Unpredictable stay length | Many expats arrive planning to stay two to three years and remain for fifteen. A short-horizon strategy looks very different from a long-term one. |

| Unregulated advisory market | The UAE does not restrict who may use the title “financial advisor.” This makes unsuitable product sales a genuine and well-documented risk. |

| Cross-border tax exposure | A home country may still tax income, assets, or estates even when an individual lives abroad full time. |

The IMF estimates UAE GDP growth at 4.8% in 2025, with the non-oil sector expanding at 6.1%. This is a strong economic environment. Growth in the broader market, however, does not automatically translate into personal wealth without a deliberate strategy behind it.

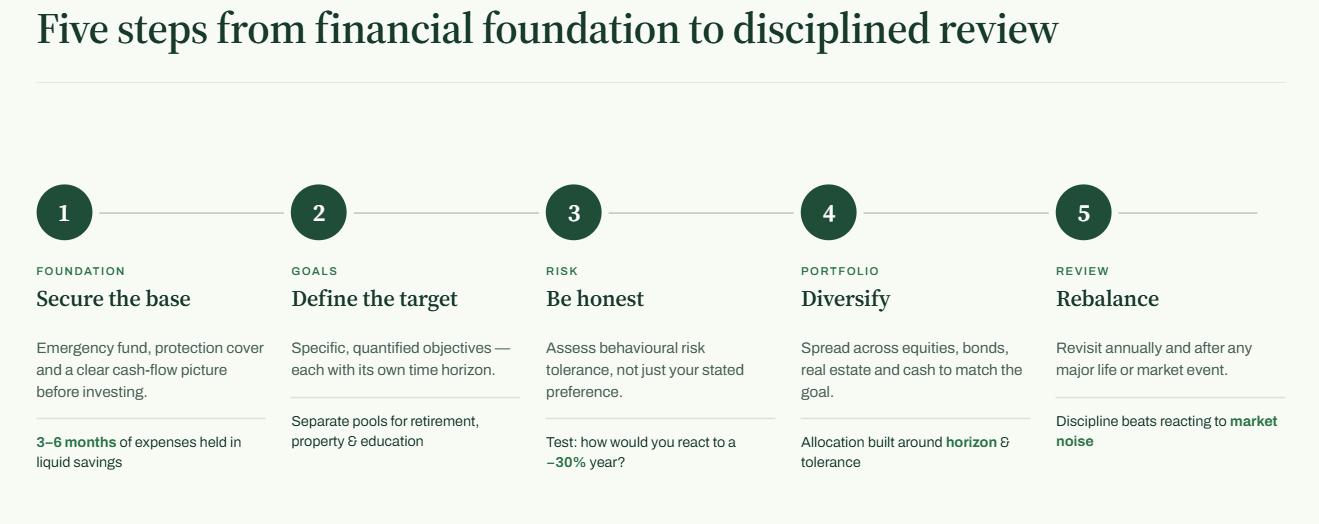

The 5-Step Investment Planning Framework for Dubai Expats

The five-step framework below provides a practical roadmap to help you invest with confidence while avoiding the mistakes that commonly erode returns.

Step 1: Build the Financial Foundation Before Investing

Investment returns compound over time. Unfortunately, so do financial mistakes. Before placing capital into any market, the foundational elements of a financial plan need to be in place.

Emergency Fund

Maintain three to six months of living expenses in liquid, accessible savings. UAE visa status is directly tied to employment. A sudden job change or termination can create significant time pressure. Expats who are forced to liquidate investments at short notice frequently do so at the worst possible moment in the market cycle.

Protection Cover

Life insurance, critical illness cover, and income protection are not optional for those with dependants or financial obligations in their home country. One serious health event without adequate cover can erase years of accumulated investment progress.

Clear Cash Flow Visibility

Establish the actual monthly surplus available for investment. This is the real figure remaining after all expenses, not an estimate. Dubai’s cost of living is high, and many professionals significantly overestimate their savings capacity until they map their cash flows in detail.

Finwiserr’s financial advisory services include structured cash flow planning as a core component. This helps clients establish accurate numbers before committing to any investment strategy.

Step 2: Define Specific and Measurable Investment Goals

Investment planning without a defined goal is speculation rather than strategy. Before selecting any asset class or product, an investor needs to know precisely what they are investing for, how much will be required, and when it will be needed.

| Goal | Typical Time Horizon | Key Consideration |

| Retirement | 15 to 30 years | No UAE state pension. Personal savings must fund retirement entirely. |

| Property purchase | 3 to 10 years | Tax implications differ significantly depending on whether the property is in the UAE, the home country, or a third location. |

| Children’s education | 5 to 15 years | International school fees in the UAE are substantial. University costs abroad add a further significant liability. |

| Financial independence | 10 to 20 years | Building passive income sufficient to make full-time employment optional. |

| Business investment | Varies | Capital deployment for business growth requires separate financial modelling and feasibility analysis. |

Each goal demands a different asset mix, liquidity profile, and level of risk. A portfolio designed for a goal twenty years away looks fundamentally different from one intended to fund school fees in three years. Treating them as a single pool of capital without a clear separation is one of the most common and costly planning errors.

For business owners evaluating capital allocation decisions, Finwiserr’s investment advisory services and corporate financial advisory can help structure both personal and business-level frameworks within a single, coordinated strategy.

Step 3: Assess Risk Tolerance Honestly

Most investors have a higher stated risk tolerance than their actual behavioural one. In practice, they express comfort with volatility until their portfolio falls 25% in a quarter. At that point, many sell at precisely the wrong moment.

A useful and direct assessment: consider how you would respond if your portfolio fell 30% in value over the next twelve months.

| Response | What It Indicates |

| You would hold and continue investing | Moderate to high risk tolerance |

| You would increase contributions to buy at lower prices | High risk tolerance |

| You would reduce or exit your position | Lower risk tolerance than previously assumed |

An honest answer to this question is more informative than any formal questionnaire.

For Dubai expats, risk tolerance is also shaped by employment stability. A professional in a long-term, stable role has a greater capacity to absorb short-term portfolio volatility than someone in a project-based or cyclical sector where income itself carries uncertainty.

Step 4: Build a Diversified Investment Portfolio

A well-constructed portfolio for a Dubai expat typically draws on multiple asset classes. The weighting across those classes depends on goals, time horizon, and risk tolerance.

Global Equities

For goals with a horizon of ten or more years, broadly diversified equity exposure through low-cost exchange-traded funds (ETFs) has historically produced the strongest real returns of any major asset class. The MSCI UAE Index delivered a return of 20.66% year-to-date in 2025, a level of local market performance that many expats overlook when focusing exclusively on global funds.

For global diversification, Ireland-domiciled ETFs are widely used by non-US investors because of their tax-efficient structure. Keeping management costs low is important. High ongoing charge figures act as a silent and compounding drag on long-term returns.

UAE Local Markets

Dubai’s IPOs raised over $9.4 billion over the past three years. The Dubai Financial Market added 230,000 new investors during that period. The UAE operates three exchanges: the Dubai Financial Market (DFM), the Abu Dhabi Securities Exchange (ADX), and Nasdaq Dubai. These provide direct access to a growing local economy with strong non-oil sector momentum.

Real Estate

Real estate is among the most popular asset classes for Dubai-based expats. Average gross rental yields across UAE residential property were approximately 5.27% in 2024, with prime locations such as Dubai Marina and Palm Jumeirah producing higher figures. These returns are free from property tax and rental income tax.

However, direct property ownership is illiquid and represents concentrated exposure to a single market and a single asset. It is not a substitute for a diversified portfolio. Where property forms part of an investment strategy, it should sit within a broader, balanced framework.

Real estate investment trusts (REITs) provide access to property-generated income without the concentration risk. They trade on exchanges in the same way as equities.

Fixed Income and Bonds

Bonds reduce portfolio volatility and provide a buffer during equity market downturns. For shorter-term goals or more conservative investors, a higher allocation to fixed income makes sense. For younger expats with long investment horizons, bonds typically represent a smaller portion of the overall portfolio.

Illustrative Asset Allocation by Investor Profile

| Investor Profile | Equities | Bonds and Fixed Income | Real Estate | Cash and Other |

| Conservative (short horizon or low risk tolerance) | 30% | 50% | 15% | 5% |

| Balanced (medium horizon, moderate risk tolerance) | 55% | 25% | 15% | 5% |

| Growth (long horizon, higher risk tolerance) | 75% | 10% | 10% | 5% |

These figures are illustrative frameworks only. They do not constitute personalised advice. Every allocation should be built around an individual’s specific goals, circumstances, and tax position.

Step 5: Recognise the Products That Cause Harm

Dubai’s expat investment market has a well-documented history of unsuitable product sales. Commission structures incentivise some advisors to recommend products that pay them the most rather than those that serve the client best.

| Product Type | The Problem |

| High-fee offshore savings plans | These plans typically run for 10 to 25 years. They carry heavy upfront commissions, layered annual charges, and significant surrender penalties. The combined costs can consume a material portion of total investment returns. |

| Insurance-linked investment products | These are frequently presented as straightforward investment vehicles. The insurance component adds cost and complexity without always delivering proportionate value. |

| Off-plan developer payment plans | These carry developer default risk, project delay risk, and are often priced at a premium above equivalent completed units. |

| Commission-based product recommendations | Any advisor who earns a commission from a product they recommend has a structural conflict of interest. This conflict exists regardless of whether the product is technically suitable. |

The rule to follow is consistent and simple. Always request a full written fee disclosure before committing to any product or service. A qualified, fee-based advisor will provide this immediately and without hesitation.

For a full framework on evaluating financial advisors in the UAE, including the specific qualifications to look for and the questions every client should ask before signing anything, read Finwiserr’s guide to financial advisors in Dubai.

Cross-Border Considerations: The Home Country Still Has a Claim

The UAE levies no personal income tax. However, the home country of an expat may still have a legal claim on income, investments, or estate assets depending on tax residency status, citizenship rules, and the types of assets held.

| Nationality | Key Cross-Border Issue |

| UK citizens | UK-domiciled individuals remain liable for UK inheritance tax on worldwide assets even when living abroad. Decisions around transferring UK pensions overseas through QROPS structures require specialist advice before any action is taken. |

| US citizens | US citizens are taxed on worldwide income regardless of residence. FBAR reporting requirements, FATCA compliance obligations, and investment restrictions on certain overseas funds apply in full. |

| Indian nationals (NRIs) | India’s FEMA regulations govern how NRIs manage overseas assets. NRI investment accounts, remittance planning, and returning resident obligations all require specific attention. |

| All other nationalities | It is important to confirm whether a home country operates residence-based or citizenship-based taxation and whether a tax treaty exists between that country and the UAE. |

Cross-border financial planning is a genuine speciality. Generic investment advice that ignores home-country tax obligations can create compliance problems and significant missed opportunities for optimisation. Professional advisory adds clear and measurable value in this area.

When to Review and Rebalance Your Portfolio

A set-and-forget approach is one of the most common and costly errors in expat investment planning. Markets shift. Personal circumstances evolve. The portfolio that was appropriate two years ago may no longer reflect current goals or risk tolerance.

| Review Trigger | Recommended Action |

| Annually | Complete portfolio review. Check allocation drift. Reassess goals and time horizons. Rebalance where needed. |

| Job change or significant salary increase | Revisit savings rate and available investment capacity. |

| Marriage, new child, or new dependent | Review protection cover and estate planning arrangements. |

| Planned relocation | Restructure portfolio to reflect the tax and regulatory environment of the destination country. |

| Major market movement (20% or more in either direction) | Assess whether target allocation has drifted and whether rebalancing is appropriate. |

The discipline to review and rebalance systematically, rather than react to short-term market noise, is one of the most consistent differentiators between successful long-term investors and those who underperform their own portfolios.

The Role of a Fee-Based Financial Advisor

Building and managing an investment portfolio as a Dubai expat involves genuine complexity. Cross-border tax considerations, currency dynamics, retirement planning without a state pension, and a product market that carries real risks all require careful handling.

A fee-based financial advisor charges clients directly for their advice. This is structurally different from an advisor who earns commissions from the products they recommend. The fee-based model aligns the advisor’s incentives with the client’s outcomes.

A qualified fee-based advisor will help clients do the following.

Define goals in investable terms. Translating life objectives into specific financial targets with realistic timelines and required returns.

Build a suitable asset allocation. Structuring a portfolio matched to risk tolerance, investment horizon, and currency considerations.

Select appropriate investment vehicles. Identifying low-cost, transparent options that serve the client’s strategy rather than the advisor’s revenue.

Manage cross-border complexity. Addressing pension decisions, tax residency questions, and compliance obligations across multiple jurisdictions.

Review and adapt the plan. Revisiting the strategy as circumstances change, rather than leaving it static.

For business owners, personal financial planning and corporate financial strategy are most effective when addressed together rather than in isolation.

Finwiserr’s advisory services cover financial advisory, investment advisory, corporate financial advisory, and project finance advisory. Personal and business financial planning can be addressed within a single, coordinated engagement.

For business owners assessing a new venture before deploying capital, Finwiserr’s financial feasibility study services for the UAE provide the structured analysis required before a significant commitment is made.

Summary

| Step | What to Do |

| 1. Foundation | Emergency fund of three to six months. Adequate protection cover. Accurate cash flow picture. |

| 2. Goals | Specific, quantified targets with defined time horizons for each objective. |

| 3. Risk | Honest assessment of behavioural risk tolerance based on actual responses rather than stated preferences. |

| 4. Portfolio | Diversified across asset classes with allocation matched to individual goals and timeline. |

| 5. Red flags | Avoid high-fee offshore products. Request written fee disclosure before signing any agreement. |

| 6. Cross-border | Confirm home-country tax obligations. Do not assume the UAE’s zero-tax position represents the complete picture. |

| 7. Review | Conduct a full review annually and following any significant life event. |

The UAE’s tax-free environment is a genuine and powerful wealth-building advantage. It produces results, however, only for those who approach it with structure and discipline. The expats who leave Dubai substantially wealthier than when they arrived are not always the highest earners. They are the ones who planned with care, avoided the most common mistakes, and worked with advisors whose interests were genuinely aligned with their own.

Speak With a Finwiserr Advisor