In the last decade, a new breed of fast-growth companies has rewritten the rules of capitalism. Firms like Tesla, Snowflake, Shopify, and Spotify have challenged how investors think about intrinsic value, often achieving multi-billion-dollar company valuations years before turning a profit. Between 2020 and 2023 alone, more than 150 global startups crossed the $1 billion valuation mark without showing positive earnings — proof that growth, not profitability, drives today’s markets.

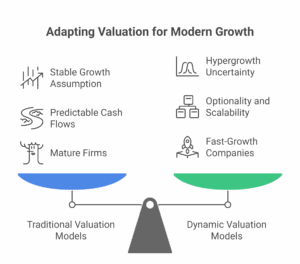

Traditional valuation models such as the Discounted Cash Flow (DCF) or P/E ratio were built for stability — companies with steady cash flows, predictable costs, and clear industry benchmarks. But fast-growth businesses move at a speed those frameworks struggle to capture. When a firm doubles its revenue every year or scales across continents in months, assumptions about margins, capital structure, and risk become outdated almost instantly.

Take Tesla as an example. In early 2020, its market capitalization was around $80 billion; by 2021, it had surged past $1 trillion, despite delivering only a fraction of the vehicles produced by legacy automakers. Traditional analysts found the math hard to justify — yet the market was valuing not just its present cash flows, but its innovation premium and growth optionality. Similarly, Snowflake, a cloud-data company with less than $600 million in annual revenue during its IPO year, debuted at a valuation of over $70 billion. These cases exposed how conventional valuation analysis struggles when faced with exponential scalability and intangible assets.

At Fin-Wiser, we call this the “growth-valuation paradox” — when future potential outweighs historical performance. Our financial modeling and valuation services are built to bridge that gap, combining traditional frameworks like DCF modeling with scenario-based forecasting that captures uncertainty and speed.

And for investors and analysts who want to experiment hands-on, the Fin-Wiser Online Store offers dynamic startup valuation tools, growth-adjusted DCF templates, and sensitivity models designed for modern, fast-changing businesses.

The valuation puzzle today isn’t about whether growth is good — it’s about how to measure it fairly. The next sections break down why classic metrics fall short, how fast-growth companies reshape valuation logic, and what analysts must do to keep up with this new era of velocity.

Traditional Valuation Models — Built for Stability, Not Speed

Most traditional valuation models were designed for companies that grow in straight lines, not rocket paths. Tools like the Discounted Cash Flow (DCF) model, Price-to-Earnings (P/E) ratio, and Enterprise Value-to-EBITDA (EV/EBITDA) multiples assume predictable margins, stable risk profiles, and consistent growth rates — the very qualities that fast-growth companies lack.

In their original form, these valuation frameworks work beautifully for mature firms like Coca-Cola, Procter & Gamble, or Johnson & Johnson, where revenues, costs, and dividends follow steady historical patterns. The DCF model can comfortably project cash flow forecasts 5–10 years ahead because volatility is low and market cycles are slow.

But apply the same approach to companies like Rivian, Shopify, or Spotify, and the math starts breaking down. A 20% change in assumptions about revenue growth or cost of capital can swing the intrinsic value by billions. In high-velocity markets, traditional models underestimate optionality, network effects, and scalability, while overestimating the predictability of cash flows.

Consider Amazon in its early years — for over a decade it posted negligible profits, yet investors valued it far higher than most retailers combined. Why? Because traditional valuation analysis couldn’t fully capture compounding ecosystem value: the idea that short-term losses could buy long-term dominance.

At Fin-Wiser, we see this mismatch daily. Classic metrics remain foundational, but not sufficient. Our valuation and financial modeling services blend conventional methods with scenario-based models and dynamic DCF frameworks that adjust for hypergrowth uncertainty — giving a truer sense of risk-reward.

For those refining their analytical edge, the Fin-Wiser Online Store features adaptive valuation templates, high-growth company DCF models, and startup sensitivity tools that let you test how shifting inputs reshape fair value.

The truth is, traditional valuation isn’t obsolete — it’s just incomplete. In an era where data scales faster than capital, analysts must evolve their models to keep pace with the very businesses they’re trying to measure.

The Fast-Growth Phenomenon — Revenue Rockets, Profits Pending

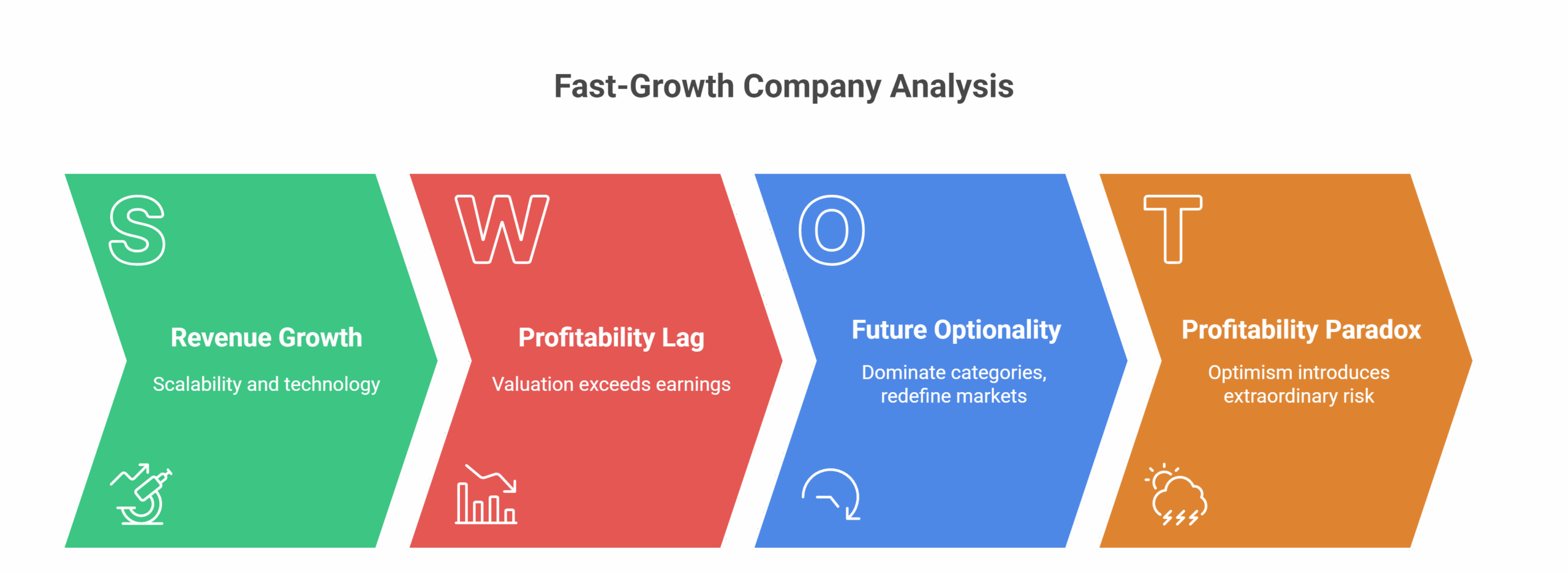

The defining trait of fast-growth companies isn’t stability — it’s acceleration. These are businesses that double, sometimes triple, their revenue growth year over year, fueled by scalability, technology, and network effects. But what makes them fascinating (and frustrating) for analysts is that their profitability often lags far behind their valuation.

In traditional corporate history, profitability was the finish line. But in today’s markets, it’s become a milestone that can wait. High-growth firms such as Uber, Spotify, and Shopify operated for years with negative earnings, yet each achieved multi-billion-dollar company valuations long before turning sustainable profits. Their value came not from current income, but from their future optionality — the ability to dominate categories, redefine markets, and eventually monetize scale.

Take Uber, for instance. By the time it went public in 2019 with a valuation exceeding $80 billion, it had never posted an annual profit. Yet investors viewed its global reach, market data, and brand dominance as future cash flow potential — metrics that don’t show up neatly in a Discounted Cash Flow (DCF) sheet. Similarly, Snowflake’s 2020 IPO at nearly $70 billion valuation came with just $264 million in annual revenue, but a staggering 120%+ revenue retention rate, signaling explosive scalability that traditional models couldn’t quantify.

This shift has created what we at Fin-Wiser call the “profitability paradox.” Investors are no longer just paying for what a company earns — they’re paying for what it could become. And while that optimism can drive extraordinary gains, it also introduces extraordinary risk.

At Fin-Wiser, our approach to valuation analysis of such businesses combines quantitative modeling with strategic foresight. Through our financial modeling services, we analyze unit economics, revenue scalability, and market penetration rates to build models that reflect both growth potential and operational reality.

For analysts and investors exploring this terrain, the Fin-Wiser Online Store offers curated high-growth DCF templates and startup valuation tools designed to handle fluctuating cash flows, dilution scenarios, and long-term scalability forecasts — the cornerstones of modern intrinsic value assessment.

In essence, fast-growth companies are redefining what “value” means. They’ve proven that market dominance and adaptability can sometimes outweigh short-term profitability — at least in the eyes of investors willing to bet on acceleration over stability.

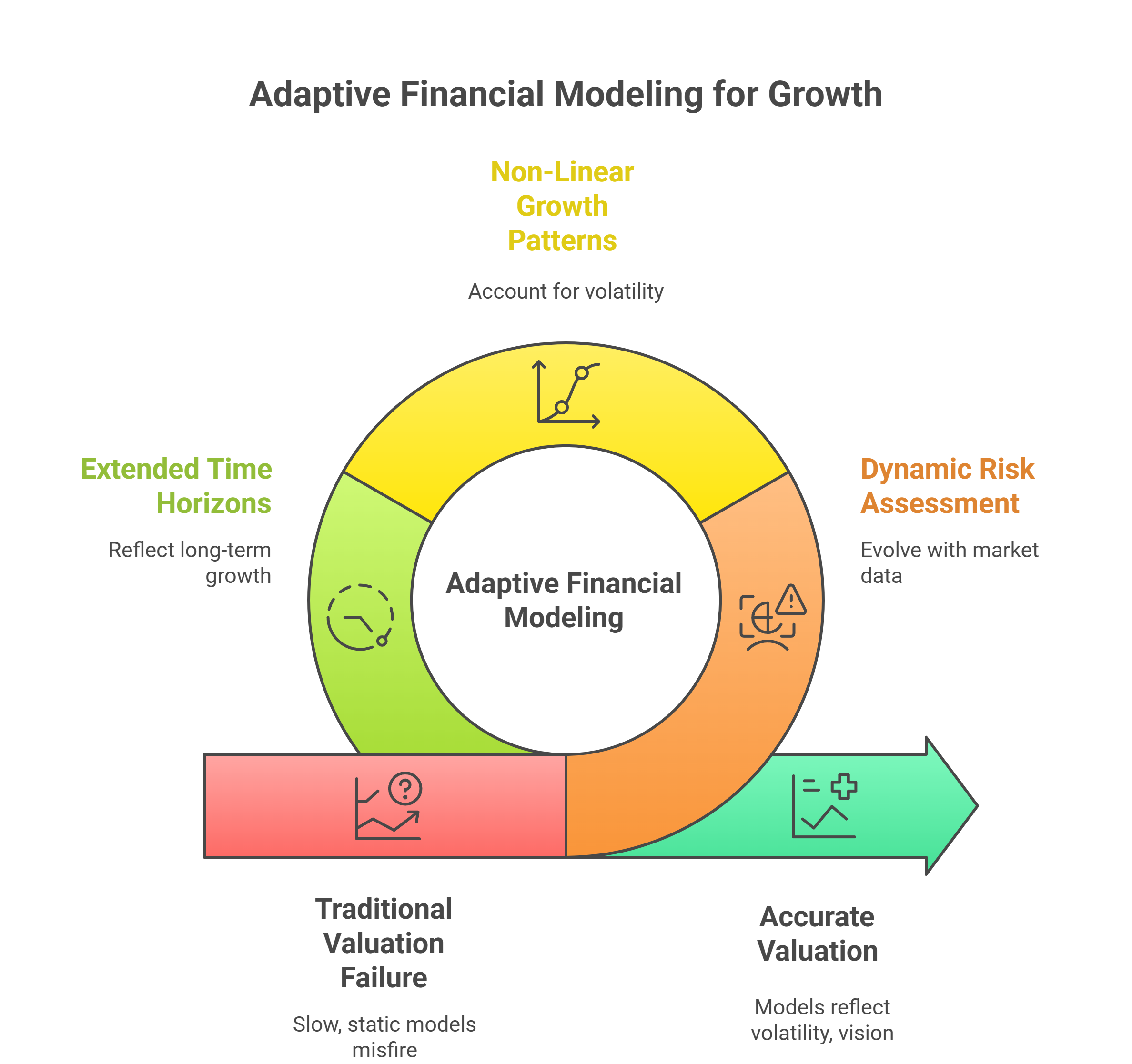

Why Metrics Misfire — Cash Flow, Risk, and Time Horizons

Traditional valuation tools struggle not because they’re wrong, but because they’re slow. The speed at which fast-growth companies evolve makes it nearly impossible for static models to keep up. The assumptions that power frameworks like Discounted Cash Flow (DCF) or EV/EBITDA break down when cash flow volatility, market uncertainty, and longer time horizons dominate the picture.

1. The Cash Flow Mirage

Most high-growth businesses reinvest every dollar back into scaling operations — whether in R&D, customer acquisition, or infrastructure. That means their free cash flow often remains negative for years. When analysts feed these volatile or negative numbers into a DCF model, it produces distorted intrinsic value results.

Consider Amazon during its early years. From 1997 to 2003, it posted losses exceeding $3 billion, yet its valuation soared because investors saw future cash flows, not current losses. Similarly, Shopify’s cash burn in the 2010s didn’t scare markets — it fueled optimism that its growth curve would justify today’s losses tomorrow.

2. The Risk Illusion

In fast-growth industries like tech, fintech, or biotech, risk changes overnight. A regulatory update, competitor pivot, or funding freeze can rewrite assumptions instantly. Traditional models assume static discount rates and predictable cost of capital (WACC) — both unrealistic in sectors where uncertainty is the norm. Analysts who fail to update their risk factors end up overvaluing businesses that operate in volatile environments.

3. The Time Horizon Trap

Classic valuation analysis typically uses a 5–10 year forecast period. But for fast-growth companies, the path to stability might take 15 or even 20 years. Using short-term horizons compresses potential and undervalues the very thing investors are paying for — the ability to grow exponentially over time.

At Fin-Wiser, we address this gap through adaptive financial modeling — frameworks that evolve with market data. Our valuation and investment services are designed to account for dynamic risk, non-linear growth patterns, and extended horizons, ensuring our models reflect both volatility and vision.

For independent professionals, the Fin-Wiser Online Store features DCF templates and scenario-based valuation models that integrate risk-adjusted projections and long-term growth simulations. These tools help analysts stress-test their assumptions against multiple futures — not just the comfortable ones.

In truth, traditional valuation metrics fail not because growth is irrational, but because they weren’t built for exponential reality. Understanding how cash flow uncertainty, risk evolution, and time horizon mismatches interact is what separates conventional analysts from forward-thinking ones — the kind of mindset that defines Fin-Wiser’s valuation philosophy.