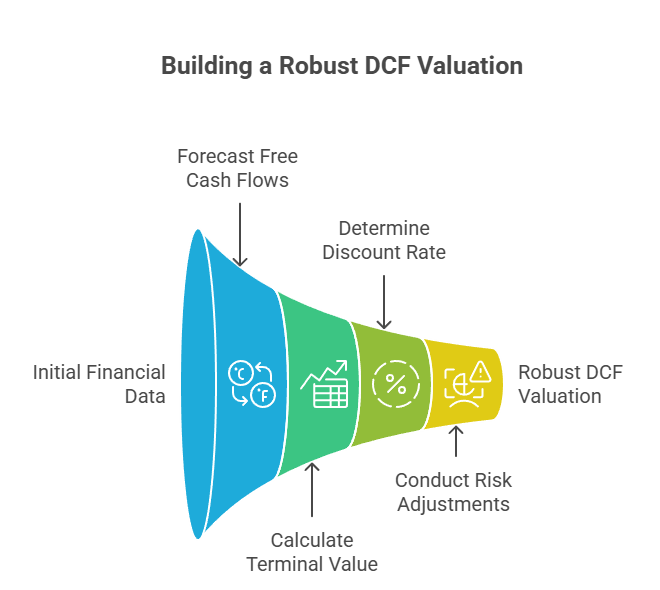

Core Elements of a Discounted Cash Flow (DCF) Valuation

Building a realistic DCF valuation means more than just plugging numbers into a spreadsheet. A robust financial modeling approach requires understanding and carefully defining the core components that drive the entire analysis. Let’s break down what you absolutely must get right to ensure your discounted cash flow calculation holds up under scrutiny from investors, lenders, or internal decision-makers.

1. Forecast Horizon and Free Cash Flow Estimation

A DCF model begins with projecting free cash flows over a defined forecast period. This period often ranges from 5 to 20+ years depending on the asset type (e.g., renewable energy projects often use 20–25 years).

Key points:

Forecast period must match asset life and revenue visibility.

Free cash flow = Operating Cash Flows – Capital Expenditures – Changes in Working Capital.

Must reflect realistic cost structures, growth patterns, and operational risks.

At Finwiserr, our financial modeling templates include structured cash flow forecasting modules that handle detailed OpEx, CapEx, and working capital adjustments, making your free cash flow projections credible and investor-ready.

2. Terminal Value Calculation

After the explicit forecast period, a DCF model typically includes a terminal value to capture remaining cash flows into perpetuity. This is often where models become overly optimistic or imprecise.

Two common methods:

Perpetuity Growth Model: Assumes cash flows grow at a stable rate forever (typically 1–3%).

Exit Multiple Method: Applies a valuation multiple to final-year metrics (e.g., EBITDA).

Critical considerations:

Use conservative, justifiable growth rates.

Align multiples with market comparables, not wishful thinking.

Finwiserr’s templates include built-in terminal value calculators that help you test both methods and avoid misleading valuations.

3. Discount Rate (WACC or Required Return)

The discount rate reflects the time value of money and project risk. Get it wrong, and your valuation can be dramatically skewed.

For companies and projects:

Use Weighted Average Cost of Capital (WACC) for enterprise valuations.

Include cost of debt, cost of equity, and appropriate capital structure.

Adjust for country risk premiums or project-specific risk factors.

Why it matters:

A model using an unrealistic discount rate will misrepresent risk and mislead decision-makers.

Finwiserr’s financial modeling solutions help users calculate WACC systematically, including debt-equity ratios and cost-of-capital inputs, ensuring your discount rate is both defensible and transparent.

4. Risk Adjustments and Scenario Planning

No single set of assumptions captures the uncertainty of the real world. Investors expect to see scenarios and sensitivities that reveal how the valuation changes with key variables.

Best practice:

Model base, downside, and upside cases.

Test sensitivities on revenue growth, discount rate, CapEx, and OpEx.

Show how these changes impact NPV and IRR.

Finwiserr’s models come with built-in scenario analysis and sensitivity tools, making it easy to test and communicate risk to stakeholders.

In short, a winning DCF valuation is built on credible free cash flow forecasts, a carefully chosen terminal value, a well-calculated discount rate, and rigorous scenario testing. These are not optional extras—they are the foundation of professional-grade financial modeling that stands up to investor scrutiny.

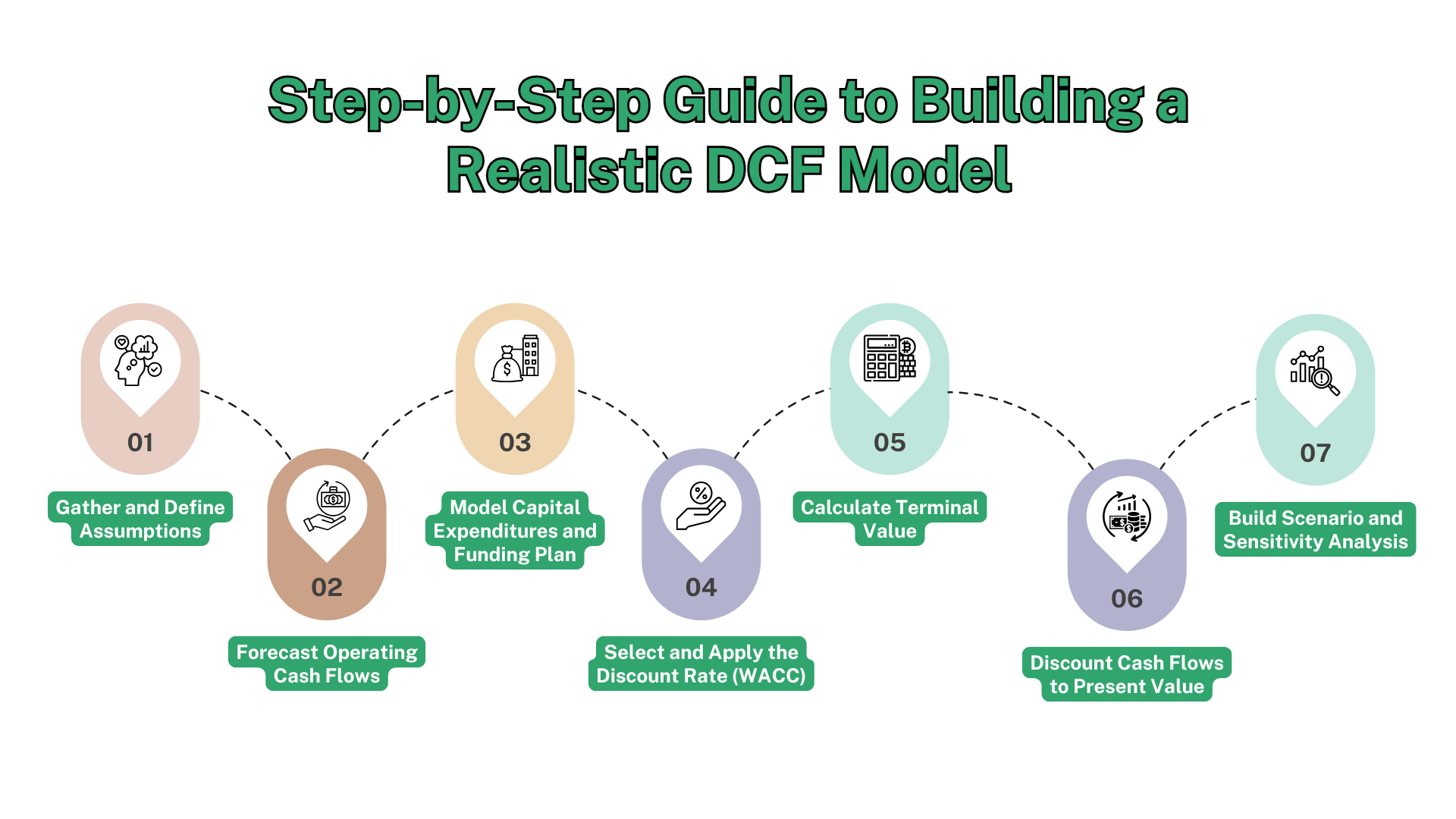

Step-by-Step Guide to Building a Realistic DCF Model

Now that we know the core elements of a discounted cash flow valuation, let’s walk through how to actually build one step by step. This process is essential whether you’re valuing a renewable energy project, a corporate acquisition target, or an infrastructure concession.

A realistic DCF model must go beyond surface-level inputs to deliver transparent, credible, and investor-friendly results. Here’s how you do it right:

Step 1: Gather and Define Assumptions

The first step in any financial modeling exercise is defining clear, justifiable assumptions:

Revenue drivers (e.g., tariffs, volume, pricing)

Operating expenses (fixed and variable)

Capital expenditures and maintenance schedules

Working capital needs

Financing structure (debt, equity, interest rates)

These assumptions should be grounded in market data, contracts, or industry benchmarks. Overly optimistic inputs are the number one reason DCF models fail under investor scrutiny.

Finwiserr’s financial modeling templates include structured assumption sheets that make inputs transparent and auditable for stakeholders.

Step 2: Forecast Operating Cash Flows

Once assumptions are defined, forecast free cash flow over the planning horizon:

Revenue = Price x Volume, adjusted for escalation or degradation.

Operating expenses with realistic escalation.

Taxes, subsidies, or grants where applicable.

Working capital changes, especially in corporate or industrial models.

CapEx timing aligned to construction or expansion phases.

A quality model links these drivers logically, ensuring internal consistency.

At Finwiserr, our templates feature fully linked financial statements so cash flow forecasting automatically adjusts to input changes.

Step 3: Model Capital Expenditures and Funding Plan

CapEx is critical in project finance modeling, especially for energy and infrastructure projects with high upfront costs. Your model should:

Phase CapEx over construction periods.

Align debt drawdowns and equity injections with spending.

Model interest during construction and grace periods.

Why this matters:

Misaligning funding and CapEx can distort cash flow timing and debt service coverage ratios.

Finwiserr’s models include automated CapEx scheduling and funding logic that eliminates manual errors.

Step 4: Select and Apply the Discount Rate (WACC)

Choosing the right discount rate is central to a realistic DCF.

Calculate WACC = Weighted Average Cost of Capital.

Include cost of equity (CAPM approach) and after-tax cost of debt.

Adjust for country or project-specific risk premiums.

Pro Tip: Always document and justify your discount rate calculation in your model.

Finwiserr’s templates come with built-in WACC calculators so you can adapt rates quickly for different projects or scenarios.

Step 5: Calculate Terminal Value

Terminal value often accounts for 50–70% of total DCF valuation. This step requires care:

Perpetuity Growth Method: Apply conservative growth rates (1–3%).

Exit Multiple Method: Use market comparables for final-year EBITDA or cash flow.

Always test the impact of different terminal growth rates on the final valuation.

Finwiserr models include terminal value calculation modules for both methods, making it easy to compare approaches.

Step 6: Discount Cash Flows to Present Value

With free cash flows and terminal value defined:

Apply discount rate to each year’s cash flow.

Sum the present values to arrive at Net Present Value (NPV).

Calculate IRR to show the implied project return.

Professional models also include Equity IRR when debt is used, giving investors a clear view of leverage impact.

Step 7: Build Scenario and Sensitivity Analysis

A realistic model doesn’t stop at a single outcome. Investors want to see how valuation shifts with changes in:

Revenue growth or tariffs

CapEx overruns

Operating cost escalation

Discount rate variations

Finwiserr’s financial modeling solutions feature built-in scenario toggles and sensitivity tables, enabling users to test downside, base, and upside cases instantly.

By following these steps carefully, you’ll avoid the common pitfalls of DCF valuation—like unjustified growth rates, inconsistent cash flow timing, or unrealistic discount rates. Instead, you’ll deliver a transparent, defendable, investor-ready valuation that builds confidence and supports strategic decisions.

How Finwiserr Helps You Build Accurate, Investor-Ready DCF Valuations

Creating a realistic DCF valuation isn’t just about math—it’s about telling a compelling, credible financial story that investors, lenders, and boards believe. And for many professionals, building that level of analysis from scratch can be daunting, error-prone, and time-consuming.

That’s exactly where Finwiserr steps in. Our financial modeling templates are built to take you from blank Excel sheets to investor-ready models with speed, precision, and confidence.

✔ Purpose-Built for DCF Valuation

Our templates are designed specifically for projects and companies that rely on discounted cash flow analysis to determine value. Whether you’re modeling a renewable energy plant, infrastructure PPP, corporate acquisition, or growth-stage startup, Finwiserr’s models include:

Structured free cash flow forecasting with linked assumptions

Automated terminal value calculators (perpetuity growth and exit multiple)

Built-in WACC calculators with cost-of-equity and debt inputs

Dynamic NPV and IRR outputs instantly updated with every change

This means you don’t just calculate DCF valuation—you own the process, fully understanding and controlling every input.

✔ Transparency and Audit-Readiness

One of the biggest mistakes in financial modeling is creating black-box spreadsheets investors can’t trust. Finwiserr’s templates prioritize:

Clearly labeled assumption sheets

Traceable, linked calculations

Built-in documentation fields

These features help you defend your discounted cash flow valuation in due diligence meetings, investment committee reviews, or bank loan negotiations.

✔ Scenario and Sensitivity Analysis Built-In

Professional-grade valuations don’t stop at a single case. Investors demand to see downside, base, and upside scenarios—and test key variables like:

Revenue growth or tariffs

Operating costs and escalation rates

CapEx overrun risk

Discount rate changes

Finwiserr’s models come with pre-built scenario toggles and sensitivity tables, so you can instantly demonstrate how robust your valuation remains under uncertainty.

✔ Faster, More Reliable Workflows

Without a solid structure, building a DCF model from scratch can take 40–80 hours, with constant risks of formula errors and logic breaks. Finwiserr’s financial modeling templates let you:

Save weeks of modeling time

Eliminate critical spreadsheet errors

Focus on strategy and decision-making instead of formulas

This efficiency is why so many developers, CFOs, and advisors rely on Finwiserr to standardize their modeling approach.

✔ Built for Real Projects, Not Just Theory

Unlike generic templates, Finwiserr’s solutions are grounded in real transaction experience across energy, infrastructure, and corporate finance. They’re designed to:

Support bankable project finance deals with full debt structuring

Handle long-term cash flow forecasting (20+ years)

Calculate detailed loan repayment schedules with DSCR analysis

Provide outputs lenders and investors recognize and trust

Whether you’re a developer bidding on a solar PPP or a corporate CFO valuing an acquisition, you get tools designed to win deals and secure financing.

👉 Ready to Build Better DCF Valuations?

Don’t settle for fragile, error-prone spreadsheets that fall apart under investor questions. With Finwiserr’s financial modeling templates, you’ll deliver clear, defensible, and investor-ready DCF valuations that drive smarter decisions and faster closes.

Explore our models today and see why professionals around the world trust Finwiserr for their most important financial analyses.