In the fast-evolving world of company valuation, trends come and go — from comparable multiples to venture growth metrics — but one method still stands tall across Wall Street, London, and Singapore alike: the Discounted Cash Flow (DCF) model.

The DCF model is often hailed as the most complete tool for estimating a company’s intrinsic value. It doesn’t rely on hype, headlines, or peer comparisons; it goes straight to fundamentals — how much money a business will generate, and what that’s worth today. When applied correctly, a DCF reveals the true worth behind the price, cutting through market speculation.

Yet here’s the paradox: while nearly every financial analyst uses a DCF calculation, very few get it right. Even small errors — a slightly inflated growth assumption, an outdated discount rate, or an overconfident terminal value — can distort the valuation analysis by millions. As recent IPOs and tech valuations have shown, precision in modeling isn’t optional; it’s what separates skilled analysts from spreadsheet optimists.

At Fin-Wiser, we’ve seen how subtle financial modeling mistakes can mislead even experienced professionals. That’s why our valuation and financial modeling services emphasize clarity, data discipline, and a realistic approach to cash flow forecasting. The goal isn’t to make the numbers look impressive — it’s to make them believable.

For those building their own models, the Fin-Wiser Online Store offers ready-to-use DCF templates, valuation tools, and investment models trusted by analysts worldwide to achieve consistent, transparent, and fact-driven results.

In this guide, we’ll uncover the most common DCF mistakes analysts make, why they happen, and how to avoid them — so your next intrinsic value analysis stands up to both scrutiny and time.

Mistake #1 – Ignoring Realistic Cash Flow Projections

The heart of every Discounted Cash Flow (DCF) model is its cash flow forecast — and yet, this is where most analysts go wrong. The temptation to project sharp revenue growth or ideal profit margins often turns DCF modeling into wishful thinking rather than financial reality.

A DCF model is only as reliable as the free cash flow projections it’s built on. Analysts frequently assume straight-line growth or apply overly optimistic revenue trajectories without factoring in cyclical trends, market saturation, or macroeconomic risks. The result? An intrinsic value that looks mathematically sound but practically impossible.

Take global examples like Uber, Snap, and Peloton. Their early valuations were heavily inflated by future growth assumptions that never fully materialized. Uber’s pre-IPO valuation analysis projected rapid profitability by 2022 — yet the company only recently began approaching positive free cash flow after years of adjustments. The math was right, but the assumptions weren’t.

At Fin-Wiser, we emphasize the principle that “realistic beats perfect.” Every valuation analysis we conduct starts with data-driven forecasting, integrating historical trends, cost dynamics, and industry benchmarks. Our financial modeling services are built to keep optimism in check — replacing guesswork with grounded financial reasoning.

For independent analysts and investors, the Fin-Wiser Online Store provides practical DCF templates and cash flow modeling tools that allow you to test your assumptions against real-world volatility. Because accuracy in cash flow forecasting isn’t just a skill — it’s the foundation of every credible intrinsic value estimate.

Remember: a DCF calculation doesn’t reward imagination. It rewards precision, patience, and an honest look at how money will actually move through a business.

Mistake #2 – Using the Wrong Discount Rate

Even the most accurate cash flow projections can crumble if the discount rate isn’t right. In a Discounted Cash Flow (DCF) model, the discount rate translates future money into today’s value — it’s the heartbeat of the entire calculation. Yet, many analysts treat it as a quick plug-in rather than a carefully derived metric.

The discount rate is meant to reflect a company’s cost of capital (WACC) — the minimum return investors expect for the risk they take. However, analysts often make two critical errors: using generic rates and misjudging risk levels. A tech startup and a utility company don’t share the same risk profile, yet both are often modeled using identical rates. That’s where intrinsic value calculations begin to drift.

Another common misstep is mishandling the components of WACC — especially beta, risk-free rate, and cost of equity. For instance, using outdated risk-free rates from previous years or applying a U.S. market beta to an international company can distort results by billions in perceived value. In 2021, for example, when global interest rates were near zero, analysts who didn’t adjust their models for post-pandemic rate hikes saw valuations fall by over 30% once reality caught up.

At Fin-Wiser, we remind every analyst: the discount rate isn’t a fixed number — it’s a reflection of current market conditions and business risk. Our valuation and financial modeling services integrate updated WACC assumptions, equity risk premiums, and country risk factors, ensuring DCF models reflect real-world capital costs, not textbook constants.

And if you’re building your own models, the Fin-Wiser Online Store features advanced DCF templates preloaded with dynamic discount rate calculators — helping you adjust inputs like cost of equity, debt ratios, and tax shields in line with market updates.

Choosing the right discount rate is more than math — it’s judgment. It’s what transforms a DCF model from a spreadsheet exercise into a true reflection of business risk and reward.

Mistake #3 – Overvaluing the Terminal Value

If there’s one place where even seasoned analysts lose control of their Discounted Cash Flow (DCF) models, it’s the terminal value. This single metric often accounts for more than 60–80% of a company’s intrinsic value, meaning one small error in assumptions can completely distort the valuation outcome.

The terminal value represents all future cash flows beyond the explicit forecast period — in essence, it’s the “forever” part of your model. And while it’s tempting to use an optimistic terminal growth rate, that optimism can quietly inflate the entire DCF valuation.

A common mistake? Assuming perpetual growth rates that exceed the long-term GDP or industry averages. For instance, analysts once modeled Netflix and Zoom with 6–7% terminal growth during pandemic peaks, far above global sustainable growth levels. When the market normalized, their valuations corrected sharply, showing how a small tweak in the growth assumption can wipe billions off a company’s equity valuation.

Another pitfall is ignoring how discount rate changes impact the terminal multiple. A 1% drop in the discount rate can boost terminal value by over 10–15%. That’s why overreliance on terminal figures without sensitivity analysis often leads to inflated intrinsic value estimates.

At Fin-Wiser, we encourage analysts to see terminal value not as a magic number, but as a discipline check. Through our valuation and financial modeling services, we train clients to validate long-term assumptions against macroeconomic trends, sector life cycles, and real-world constraints — not just spreadsheet logic.

For analysts who prefer building their own models, the Fin-Wiser Online Store provides advanced DCF templates with built-in terminal value calculators and growth-rate sensitivity tools. These models help test how different WACC or growth assumptions affect final outcomes — ensuring that the intrinsic value you calculate stands up to professional scrutiny.

The truth is, every great DCF model needs a touch of humility. Long-term forecasts aren’t meant to predict the future; they’re meant to measure the reasonable boundaries of it. And the moment your terminal value looks too perfect — it probably is.

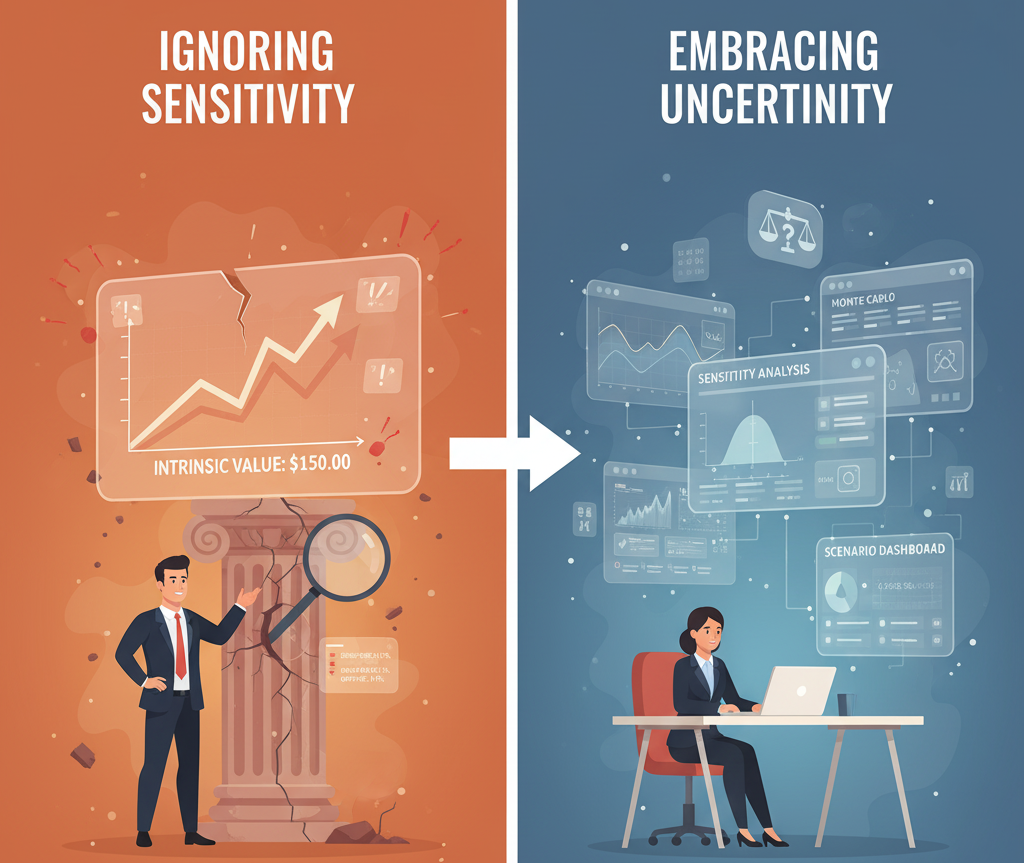

Mistake #4 – Ignoring Sensitivity and Scenario Analysis

Even the most carefully built Discounted Cash Flow (DCF) model is only as strong as its ability to handle uncertainty. Markets change, interest rates shift, and competitive dynamics evolve — yet many analysts still present a single-point intrinsic value as if it were absolute truth. This is one of the biggest blind spots in valuation analysis.

A DCF model is not meant to be static. It should show how changes in cash flow projections, discount rates, or terminal growth assumptions impact valuation outcomes. This process, known as sensitivity analysis, helps uncover the range of potential outcomes — not just the most convenient one.

Ignoring scenario testing means overlooking risk. When interest rates surged globally in 2022–2023, companies across tech and real estate saw valuations plunge by 20–40%, not because their operations collapsed, but because analysts hadn’t accounted for macro sensitivity. A simple tweak in the WACC or risk-free rate would have revealed that fragility long before markets corrected.

At Fin-Wiser, we integrate sensitivity and scenario analysis into every valuation model we build. Whether it’s testing best, base, and worst-case projections or simulating rate hikes and inflation impacts, our valuation and financial modeling services are structured to expose vulnerabilities before capital is committed.

For independent analysts, the Fin-Wiser Online Store offers professional DCF templates embedded with sensitivity tables, Monte Carlo simulators, and dynamic scenario dashboards. These tools let you instantly visualize how small assumption changes ripple through your DCF valuation, helping you move from guesswork to confidence.

In reality, valuation accuracy is never about predicting the future — it’s about preparing for it. Analysts who embrace sensitivity analysis don’t just find a number; they discover the limits of their conviction. And that’s what separates cautious professionals from careless forecasters.