Ask most analysts to run a DCF modeling exercise, and they’ll plug in revenue, cost assumptions, CAPEX, maybe a terminal growth rate—and call it a day. But in industries driven by innovation, identity, and customer experience, that model misses something huge: intangible assets valuation.

Things like brand valuation, proprietary tech, and customer loyalty aren’t just abstract concepts. They’re what make companies like Apple, Adobe, or Nike able to dominate in pricing, retention, and margin. Yet most models still leave these out—or worse, treat them like a footnote.

It’s not because they don’t matter. It’s because most people don’t know how to quantify them. This blog exists to change that.

We’ll break down the tools, numbers, and mindset you need to model intangible assets correctly. That means plugging brand, intellectual property, and customer loyalty directly into your DCF modeling framework—with data, not guesswork.

Most traditional templates won’t get you there. That’s why firms are turning to platforms like Fin-Wiser for sharper approaches and proven modeling strategies. If you’re building valuations for IP-heavy companies or SaaS businesses, start by exploring our financial advisory services or upgrade your toolkit with custom DCF templates built specifically for this use case.

To model modern businesses, you need to think beyond the balance sheet. You need to model what actually drives value.

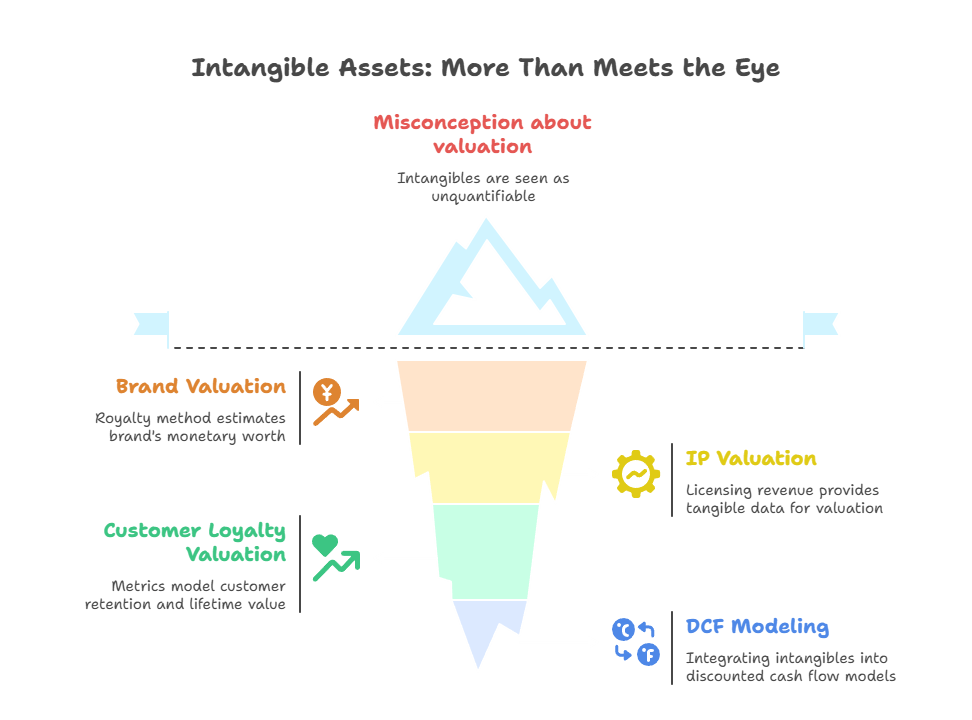

Misconception #1: “Intangibles Can’t Be Valued with Real Numbers”

One of the most common misunderstandings in intangible assets valuation is that you “can’t put a number on it.” That’s flat-out wrong. You absolutely can—and institutional investors do it all the time.

Start with brand valuation. The relief-from-royalty method is a widely accepted approach where you estimate what royalty a company would pay to license its own brand from a third party. For example, if Nike had to license the Swoosh, estimates suggest the implied royalty rate could be around 1% to 3% of revenue. When applied to billions in sales, that turns into a massive value driver. These are numbers you can model—just like any other asset.

The same goes for intellectual property valuation. For a company like Qualcomm or ARM, IP isn’t an abstract strength—it’s a licensing revenue machine. Market comparables, licensing agreements, and legal filings offer hard data that can be used to estimate fair market value.

Need help structuring that into your model? Fin-Wiser’s DCF templates are designed to make these calculations easier to integrate—especially for tech and consumer companies. And if you’re dealing with more nuanced IP structures or brand licensing issues, consider tapping into our financial advisory to get it right the first time.

Even customer loyalty valuation can be modeled using metrics like churn rate, customer lifetime value (CLTV), and retention curves. Subscription companies already do this by default—so why shouldn’t you?

Still unsure how this fits in your broader DCF modeling process? You can explore our full scope of valuation services and get clarity on how to transform abstract value into line-item forecasts.

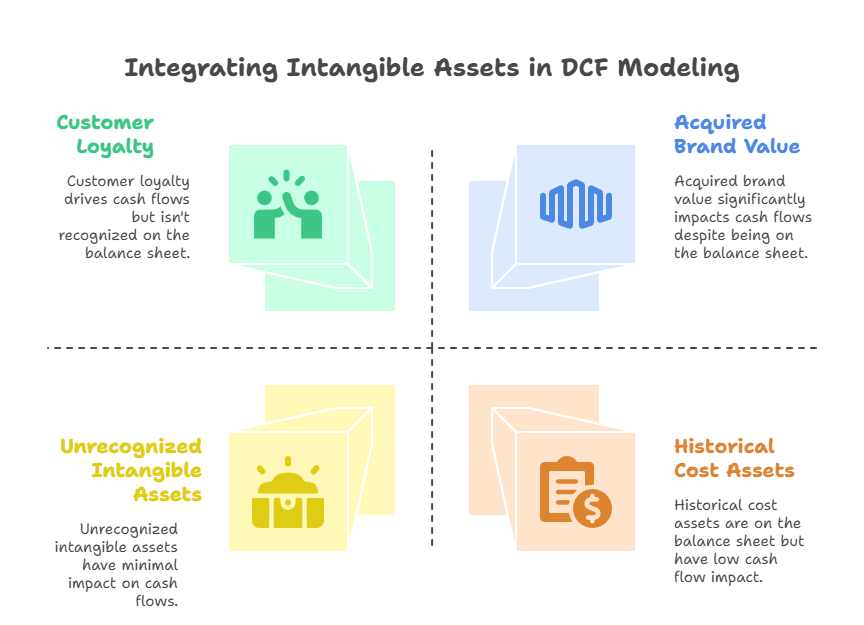

Misconception #2: “If It’s Not on the Balance Sheet, It’s Not in the Model”

A lot of people—especially early-stage analysts—think if an asset doesn’t show up under GAAP, it doesn’t belong in a DCF modeling scenario. That’s a dangerous assumption.

Just because intangible assets like brand or customer loyalty aren’t always recognized on the balance sheet doesn’t mean they don’t exist. Accounting rules are built on historical cost and strict recognition criteria. Valuation is built on future cash flows. Those are two very different things.

Take brand valuation again. Coca-Cola’s brand doesn’t show up on its balance sheet unless it was acquired—but Forbes and Interbrand estimate it’s worth over $60 billion. Why? Because it gives Coke the ability to maintain pricing power, global distribution leverage, and customer retention—all of which directly influence projected cash flows.

And what about customer loyalty valuation? Netflix, for instance, doesn’t capitalize the value of its subscriber base, but investors absolutely do. A drop in retention or a spike in churn hits valuation faster than a line-item on the balance sheet ever could.

This is why DCF modeling must go beyond what’s in the financial statements. You’re forecasting how a company will generate cash—not reciting past transactions.

If you’re unsure how to integrate unbooked intangibles into your models, check out Fin-Wiser’s services that bridge the gap between compliance and valuation strategy. You can also start with our curated DCF templates tailored to industries where intangibles matter most.

For more complex cases—especially involving tech or consumer brands—our team at Fin-Wiser can help decode what should be valued, even when the balance sheet stays silent.

Valuation is about what drives the business forward, not what’s already recorded. Don’t let accounting rules limit your strategic thinking.

Valuation Techniques That Work (And How to Use Them)

Once you accept that intangible assets valuation belongs in your model, the next question is: how?

Here are the most proven, accepted, and DCF modeling-ready approaches—used by professionals when modeling brand valuation, intellectual property, and customer loyalty into real-world forecasts.

1. Relief-from-Royalty Method

This method estimates how much a company would have to pay to license its own brand or IP from a third party. It’s perfect for brand valuation or trademarked technologies.

Let’s say a retail brand generates $500 million in annual revenue, and comparable royalty rates in the space are 2%. That implies $10 million in savings from not having to license the brand externally. Discount that stream at an appropriate rate, and you’ve got a defensible asset value.

We’ve seen clients using our financial advisory services apply this method to both household brands and niche IP portfolios—sometimes revealing hidden value that dwarfs tangible asset totals.

2. Multi-Period Excess Earnings Method (MPEEM)

MPEEM is the go-to for customer loyalty valuation. It works by isolating the cash flows attributable to one intangible—say, a subscription base—then deducting contributory asset charges (like tech infrastructure or working capital), and discounting what’s left.

For example: Adobe’s pivot to Creative Cloud wasn’t just about SaaS revenue. It also unlocked measurable stickiness, allowing the company to justify a valuation multiple north of 30x earnings. That kind of premium doesn’t come from balance sheet assets—it comes from high-retention customer value.

Need help mapping this out? Fin-Wiser’s DCF templates include real-life plug-and-play logic for subscription models, so you’re not left guessing.

3. Cost and Market Approaches (Less Common, Still Useful)

In some cases, the cost to recreate an asset—or benchmark market comps—can serve as sanity checks. These are rarely used in isolation but can be helpful for startups with fresh IP or early-stage brands.

For instance, rebuilding a proprietary AI model from scratch might cost $4 million in engineering time and compute—establishing a lower-bound estimate for intellectual property valuation.

We often work with founders and CFOs who don’t know how to model these edge cases into their forecasts. That’s where a direct consultation via Fin-Wiser can help create a full picture.